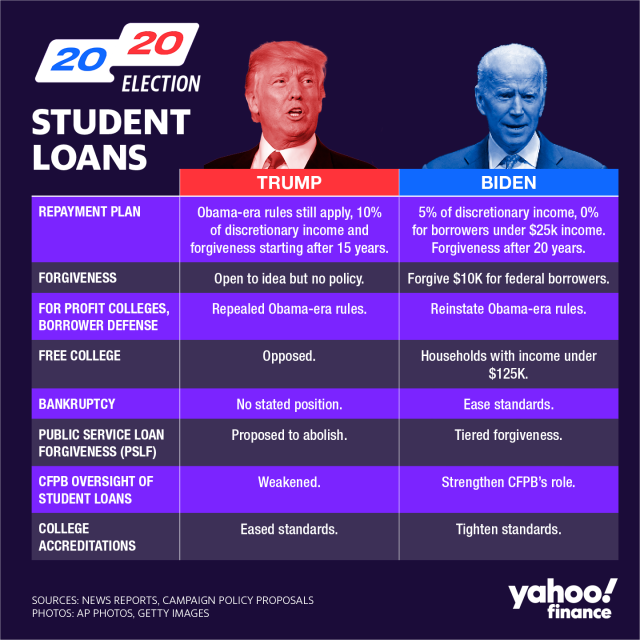

Trump Administration Expands Student Loan Forgiveness Under Income-Driven Plans

The Trump administration has reached an agreement with the American Federation of Teachers (AFT) to resume processing student loan forgiveness under key income-driven repayment plans such as Income-Contingent Repayment (ICR) and Pay As You Earn (PAYE). This deal, pending court approval, reactivates forgiveness programs paused since February 2025, benefiting over two million borrowers by reopening avenues for debt relief without triggering unexpected tax burdens. The agreement also addresses concerns raised by the federal government shutdown, which has delayed processing, and clarifies that borrowers forgiven in 2025 will not face tax liabilities on discharged debt. However, alongside this progress, the administration is exploring selling parts of the $1.6 trillion federal student loan portfolio to private investors, raising questions about borrower protections and the future role of the federal government in student lending.

Summary

The Trump administration has reached an agreement to expand student loan forgiveness programs, reopening paths for millions of borrowers to receive debt relief

The Trump administration and the American Federation of Teachers (AFT) have agreed to resume processing student loan forgiveness under several income-driven repayment plans, including the Income-Contingent Repayment (ICR) and Pay As You Earn (PAYE) programs. This agreement, pending court approval, marks a significant development in resolving disputes over paused forgiveness programs and aims to prevent borrowers from facing unexpected tax burdens. The deal follows years of stalled debt cancellations and legal challenges related to federal student loans.

- The agreement reactivates student loan forgiveness processing for eligible borrowers under the ICR and PAYE repayment plans, previously paused since February 2025.

- Over two million borrowers enrolled in Income-Based Repayment (IBR) plans have been notified of their loan forgiveness eligibility as part of the resumption effort.

- The Trump administration is also considering selling parts of the federal student loan portfolio, valued at $1.6 trillion, to private investors, raising concerns about borrower protections.

- Government shutdown and staffing issues may delay paperwork and forgiveness processing, possibly affecting borrowers’ tax liabilities due to upcoming changes in federal tax law.

- The agreement ensures that borrowers who become eligible for loan forgiveness in 2025 will not receive tax bills on discharged debt, addressing a looming "tax bomb."

Background and agreement details

The Trump administration’s accord with the American Federation of Teachers comes after months of litigation and controversy over federal loan forgiveness programs. The administration had previously paused forgiveness under income-driven repayment (IDR) plans citing court orders affecting Biden-era initiatives like the SAVE plan. These legal challenges resulted in the suspension of some forgiveness programs, leaving many borrowers in limbo.

Under the agreement, the U.S. Department of Education will resume processing loan cancellations for borrowers eligible under ICR, PAYE, IBR, and Public Service Loan Forgiveness (PSLF) programs, as long as those programs remain active. Borrowers who made payments after becoming eligible for forgiveness will be reimbursed. The deal also mandates regular progress reports to the court on application processing and loan discharges.

Eligibility and program details

The IBR repayment plan, established by Congress in 2007, ties monthly payments to a borrower’s discretionary income and family size, with forgiveness of remaining debt after 20 or 25 years of payments. The program was updated in 2014 to reduce payments as a percent of income and shorten the repayment period for newer enrollees. Borrowers can switch between income-driven plans with payments made prior to enrollment counting toward forgiveness eligibility.

Recent legislative changes under President Trump’s “big beautiful” spending bill eliminated the financial hardship requirement for enrollment and extended eligibility to some parent PLUS borrowers. As of the second quarter of 2025, approximately 2 million borrowers were enrolled in IBR plans.

Challenges from the government shutdown

Since October 1, the federal government shutdown has complicated the implementation of the loan forgiveness agreement. Federal Student Aid offices have limited capacity to maintain websites or respond to borrower inquiries. Although borrowers are advised to continue making payments, delays in paperwork and loan cancellation processing are expected due to furloughed Education Department staff.

These operational delays raise concerns about tax consequences. A 2021 American Rescue Plan provision currently exempts forgiven student debt from being taxed until the end of 2025. After this, forgiven debt may be considered taxable income, potentially burdening borrowers with large tax bills in 2026. The agreement between the Education Department and AFT clarifies that borrowers who qualify for forgiveness in 2025 will not face federal taxes on that relief.

Legal and advocacy perspectives

The AFT sued the Trump administration earlier in 2025 after the Education Department removed IDR enrollment applications and stopped processing them. The union argued that the administration unlawfully blocked access to agreed-upon forgiveness programs. AFT President Randi Weingarten described the agreement as a victory for borrowers and pledged continued advocacy for affordable higher education and debt relief.

Legal advocates like Winston Berkman-Breen emphasized that the agreement protects borrowers from unexpected tax bills caused by bureaucratic delays. Consumer groups caution, however, that the administration’s moves to roll back Biden-era forgiveness policies and restart debt collections leave many students vulnerable.

Selling federal student loans to the private market

Aside from the forgiveness agreement, senior Trump administration officials have been exploring options to sell parts of the federal student loan portfolio—totaling $1.6 trillion—to private investors. Discussions involve the Education and Treasury Departments and finance industry executives, focusing on high-performing segments of student debt owed by approximately 45 million Americans.

This strategy aligns with Republican efforts to reduce the federal role in student lending and boost private sector involvement. However, experts express concerns about the impact on borrower protections which are stronger under federal management. The government’s unique powers, such as garnishing Social Security benefits and tax refunds, would diminish under private ownership.

Experts like Preston Cooper (American Enterprise Institute) and Eileen Connor (Project on Predatory Student Lending) warn that private investors are unlikely to pay full value for the loans, potentially disadvantaging taxpayers and borrowers. Concerns also exist that only deals unfavorable to borrowers could satisfy economic criteria. Progressive groups fear sales would enrich wealthy investors at the expense of families burdened by education loans.

The path forward

The agreement between the Trump administration and AFT awaits judicial approval, which will enable the Education Department to expedite debt cancellations for eligible borrowers and prevent unexpected tax liabilities next year. The Biden-era SAVE program remains under legal uncertainty, but for now, key income-driven repayment plans continue in operation.

Meanwhile, the government shutdown and policy shifts introduce uncertainties for borrowers. The administration’s broader agenda includes reforming loan management, potentially transferring responsibilities from the Education Department to Treasury and phasing out legacy repayment plans by mid-2028.

The balance between reducing federal involvement, ensuring borrower protections, and managing taxpayer interests will shape the future of student lending in the United States, with ongoing legal, political, and financial ramifications.

Questions and answers

Q: How to qualify for student loan forgiveness 2025

A: To qualify for student loan forgiveness in 2025, borrowers generally need to meet specific criteria depending on the forgiveness program they pursue. Common programs include Public Service Loan Forgiveness (PSLF), which requires 10 years of qualifying payments while working in an eligible public service job, and income-driven repayment (IDR) plan forgiveness, typically after 20-25 years of qualifying payments. Staying current on loans, enrolling in an IDR plan when applicable, and ensuring employment in qualifying sectors are key steps. It's important to stay updated on program changes as policies may evolve.

Q: Latest updates on income-driven repayment plans

A: Recent updates to income-driven repayment (IDR) plans aim to make monthly payments more affordable by capping payments at a percentage of discretionary income and shortening forgiveness timelines. The Biden administration has introduced changes to improve IDR plans, including recalculating discretionary income to exclude more living expenses and expanding eligibility. Additionally, there have been efforts to simplify enrollment and improve borrower communication. Borrowers should review their plan details and stay informed about policy updates to maximize benefits.

Q: Effects of government shutdown on student loan processing

A: A government shutdown can disrupt student loan processing by delaying customer service, application approvals, and disbursement of funds due to reduced staff at the Department of Education. During a shutdown, federally managed loan systems may operate with limited capacity, causing delays in income-driven repayment adjustments, loan consolidation, and forgiveness processing. However, urgent services might continue in a limited fashion. Borrowers are advised to plan ahead and expect potential processing delays during such periods.

Q: Trump administration student loan policies

A: The Trump administration implemented several student loan policies focused on reducing federal involvement and promoting private sector participation. Key actions included tightening income-driven repayment plan requirements, proposing the sale of defaulted loans to private collectors, and attempting to roll back certain borrower protections. The administration also aimed to increase transparency and accountability for colleges but faced criticism for reducing loan forgiveness opportunities. Many proposed changes were moderated or reversed by subsequent administrations.

Q: Impact of federal loan portfolio sale to private investors

A: Selling federal student loan portfolios to private investors can shift loan servicing and collection responsibilities from the government to private entities. This may lead to changes in borrower experiences, including differences in repayment options, customer service, and enforcement practices. While sales can raise immediate government revenue and reduce administrative burdens, critics worry about stricter collection tactics and reduced borrower protections. The long-term impact depends on contract terms and regulatory oversight of private servicers.

Key Entities

Trump administration: The Trump administration refers to the U.S. federal government under President Donald Trump from 2017 to 2021. It was known for its conservative policies, including significant changes in education funding and regulations.

American Federation of Teachers: The American Federation of Teachers (AFT) is a major labor union representing educators and public employees in the United States. It advocates for teachers' rights, education funding, and policies supporting public education reform.

U.S. Department of Education: The U.S. Department of Education is a federal agency responsible for establishing policy on federal financial aid for education and enforcing laws related to education. It oversees programs and initiatives aimed at improving the quality and accessibility of education across the country.

Randi Weingarten: Randi Weingarten is the president of the American Federation of Teachers, leading efforts to support teachers and promote public education policies. She has been a prominent voice in education reform and labor advocacy.

Preston Cooper: Preston Cooper is a researcher and writer who frequently analyzes education policy and government spending. His work often critiques and evaluates the effectiveness of education programs and policies.

External articles

- Education Dept. Agrees to Resume More Student Loan ...

- Student loan debt will be forgiven for millions of borrowers ...

- Trump administration agrees to speed up student loan ...

YouTube Video

Title: Trump’s Student Loan Forgiveness

URL: https://www.youtube.com/shorts/iXyMAh-ISYU

Money